Author: Arran Turner, Finance Specialist at Sorbus Finance

Last updated: April 2026

Purchasing a fleet of vans represents a significant capital decision for any growing business. Whether you’re scaling delivery operations, expanding a trades workforce, or refreshing aging vehicles, financing five or more vans requires a different approach than single-vehicle purchases.

This guide covers everything mid-sized and larger businesses need to know about fleet van finance—from structuring deals that protect cash flow to leveraging tax advantages that improve your bottom line.

If you are contemplating your current options for purchasing new vehicles, we have found CarWow’s ‘Best Large Panel Vans of 2026’ a really helpful guide!

What Is Fleet Van Finance?

Fleet van finance refers to specialist funding arrangements designed for businesses acquiring multiple commercial vehicles simultaneously—typically five or more. Unlike retail motor finance, fleet arrangements account for the operational realities of running commercial vehicles at scale: staggered delivery schedules, mixed vehicle specifications, residual value management, and the administrative burden of maintaining multiple assets.

The fleet finance market in the UK has evolved considerably. Lenders now offer bespoke structures that align repayment profiles with seasonal revenue patterns, bundle maintenance into monthly costs, and provide flexibility to add or remove vehicles mid-term.

Key characteristics distinguishing fleet finance from standard vehicle loans:

- Volume-based pricing — Interest rates and fees typically decrease as fleet size increases, reflecting reduced per-unit administration costs and stronger negotiating leverage.

- Consolidated administration — Single monthly payments, unified documentation, and dedicated account management replace the complexity of managing multiple separate agreements.

- Flexible end-of-term options — Fleet agreements commonly build in choices to extend, return, part-exchange, or purchase vehicles outright, allowing businesses to respond to changing operational needs.

- Whole-life cost modelling — Fleet funders often incorporate maintenance, tyres, breakdown cover, and disposal into proposals, giving clearer visibility of true running costs.

How Does Van Fleet Finance Work With Sorbus Finance?

The mechanics of fleet van finance vary depending on the structure chosen, but the broad process follows a consistent pattern:

1. Needs Analysis and Specification

Before approaching funders, businesses define their requirements: how many vehicles, what specifications, expected mileage, contract duration, and whether services like maintenance should be bundled. This scoping phase determines which finance products suit the situation.

2. Proposal and Credit Assessment

A finance broker or direct lender prepares a proposal based on vehicle costs, residual values, and the business’s credit profile. For fleet transactions, lenders conduct more thorough due diligence than for single vehicles—reviewing filed accounts, cash flow projections, and sometimes industry-specific risk factors.

3. Agreement Structure

Once approved, the funder documents the arrangement. Fleet agreements typically specify:

- Monthly rental or repayment amounts

- Contract length (commonly 36–60 months)

- Annual mileage allowances

- Maintenance inclusions or exclusions

- Early termination terms

- End-of-contract options

4. Vehicle Procurement and Delivery

The funder either pays the supplying dealer directly or reimburses the business post-purchase. For large orders, deliveries often stagger over weeks or months—fleet finance structures accommodate this with flexible start dates or phased billing.

5. Ongoing Management

Throughout the contract, businesses make regular payments and manage vehicles within agreed parameters. Fleet funders provide online portals for tracking assets, scheduling services, and handling disposal at term end.

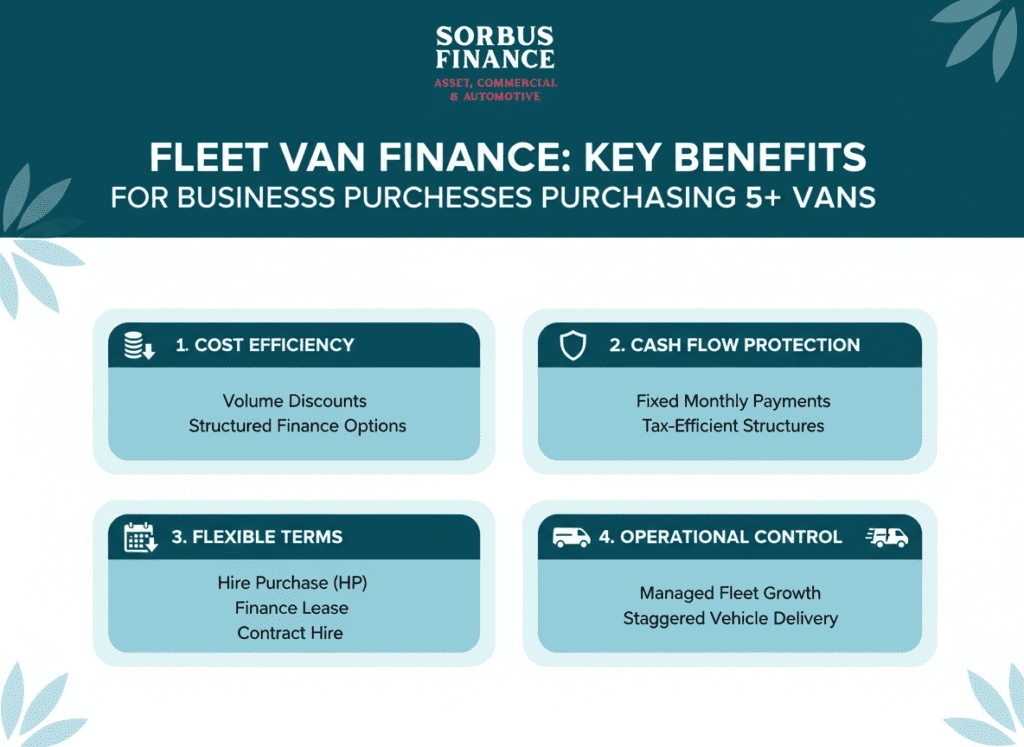

What Are the Main Types of Fleet Van Finance?

Businesses financing five or more vans typically choose from four primary structures. Each carries distinct accounting, tax, and operational implications.

Hire Purchase (HP)

With hire purchase, the business pays a deposit followed by fixed monthly instalments over an agreed term. Ownership transfers automatically once the final payment clears.

How it works: The finance company purchases the vans and “hires” them to the business. Monthly payments cover the vehicle cost plus interest, spread evenly across the contract. A nominal option-to-purchase fee (often £1) completes the transfer.

Balance sheet treatment: Vans appear as assets on the business balance sheet from day one, with the outstanding finance recorded as a liability.

Tax position: The business claims capital allowances on the vehicle’s purchase price. For vans, the Annual Investment Allowance (AIA) typically permits 100% first-year deductions up to the £1 million threshold—a significant advantage for fleet purchases.

Best suited to: Businesses wanting eventual ownership, those prioritising capital allowance claims, and organisations comfortable with asset-based balance sheet growth.

Finance Lease

A finance lease gives the business use of vehicles for most of their useful life, with rentals calculated to recover the full capital cost plus interest. The funder retains legal ownership throughout.

How it works: Monthly rentals are fixed for the primary period (usually 3–5 years). At contract end, the business either returns the vehicles or arranges a secondary rental at a reduced rate. Some leases allow the business to share in sale proceeds if residual values exceed projections.

Balance sheet treatment: Under IFRS 16 and FRS 102, finance leases are capitalised—the asset and corresponding liability both appear on the balance sheet, similar to hire purchase.

Tax position: Rentals are not directly deductible; instead, the business claims capital allowances on the capitalised asset value.

Best suited to: Businesses wanting balance sheet assets without ownership obligations, and those comfortable with fixed terms.

Operating Lease (Contract Hire)

Operating leases—commonly called contract hire—cover a shorter portion of the vehicle’s useful life. Monthly rentals are set against expected depreciation plus funding costs, with the funder bearing residual value risk.

How it works: The business agrees a contract length and annual mileage. Rentals reflect the difference between purchase price and anticipated resale value at term end, plus interest. Maintenance packages are often bundled in. At contract conclusion, vehicles return to the funder.

Balance sheet treatment: Operating leases traditionally sat off-balance-sheet. Under IFRS 16, most leases now require capitalisation, though exemptions remain for short-term and low-value assets.

Tax position: The full rental payment (excluding any non-qualifying elements like maintenance) is typically deductible as an operating expense, simplifying tax accounting.

Best suited to: Businesses prioritising predictable monthly costs, those wanting no residual value exposure, and organisations replacing fleets on fixed cycles.

Outright Purchase with Asset Finance

Some businesses prefer direct ownership from the outset, funding vehicle purchases through term loans, revolving facilities, or general working capital lines.

How it works: The business buys vehicles outright and owns them immediately. Finance may come from a secured or unsecured business loan, an existing credit facility, or cash reserves.

Balance sheet treatment: Vehicles appear as fixed assets; any borrowing appears as a liability.

Tax position: Full capital allowance claims apply, identical to hire purchase.

Best suited to: Cash-rich businesses, those with existing favourable credit lines, and organisations prioritising complete flexibility over structured vehicle finance.

What Are the Benefits of Using a Finance Broker for Fleet Van Purchases?

Arranging finance for multiple vehicles introduces complexity that single-vehicle transactions don’t carry. Working with a specialist broker provides advantages at each stage.

Access to the Whole Market

Banks and captive lenders (manufacturer finance arms) each serve specific segments. A broker maintains relationships across multiple funders—high-street banks, specialist asset financiers, challenger lenders, and manufacturer programmes—comparing terms to identify the best fit.

For fleet transactions, this matters more than for single vehicles. Funder appetite varies by industry, vehicle type, and deal size. A broker knows which lenders are actively seeking fleet business and which offer the strongest terms for specific circumstances.

Expertise in Deal Structuring

Fleet finance involves more variables than standard car loans: staggered deliveries, mixed specifications, seasonal payment profiles, and maintenance inclusions all affect pricing and documentation.

Brokers experienced in commercial vehicle fleets understand how to structure deals that align with cash flow patterns—for example, lower payments during quieter trading months, or balloon payments timed to coincide with annual bonuses or contract renewals.

Negotiating Leverage

Volume carries weight in finance negotiations. Brokers placing significant business through funders hold leverage that individual businesses typically lack. This translates to margin reductions, fee waivers, and more favourable terms.

Administrative Efficiency

For finance teams already stretched, managing a competitive tender across multiple lenders absorbs significant resource. A broker handles proposal requests, compiles comparisons, negotiates terms, and coordinates documentation—freeing internal teams to focus on core operations.

Ongoing Relationship Management

At Sorbus Finance, we believe good finance brokers maintain relationships beyond initial transactions. They monitor market conditions, flag refinancing opportunities when rates shift, and support end-of-term decisions.

How Much Does It Cost to Finance a Fleet of Vans?

Fleet finance costs depend on multiple factors that interact in complex ways. Understanding these drivers helps businesses evaluate proposals effectively.

Vehicle List Price and Discounts

The starting point is vehicle cost. Fleet orders typically attract manufacturer discounts unavailable to retail buyers—often 15–25% below list price for volume commitments. These discounts reduce the capital amount financed, directly lowering monthly payments.

Deposit or Advance Payment

Deposit options and initial rentals vary from customer to customer. With a Finance Lease or Contract Hire agreement initial rentals are commonly expressed as a multiple of monthly rentals (e.g., “3+35” indicates three months’ advance plus 35 monthly payments). Higher deposits reduce ongoing payments but require greater initial cash outlay. Hire Purchase agreements often have the VAT element of the purchase paid in advance and then any addition deposit on top. If you are making larger purchases, a VAT deferral may be appropriate.

Interest Rate (APR or Flat Rate)

Rates vary by lender, deal size, credit profile, and prevailing market conditions. Fleet transactions often secure preferential rates due to reduced per-unit administration and perceived lower risk from established businesses.

As of early 2025, competitive fleet finance rates for creditworthy businesses typically range from 5–9% APR, though specialist sectors or weaker credits may see higher pricing.

Contract Length

Longer contracts spread costs over more payments, reducing monthly amounts but increasing total interest paid. Most fleet van finance runs 36–60 months; shorter terms preserve equity but demand higher cash flow.

Mileage Allowance

For leases, contracted mileage affects pricing. Higher mileages increase expected depreciation, raising rentals. Underestimating mileage risks excess charges at contract end; overestimating means paying for unused allowance.

Maintenance Inclusion

Bundled maintenance packages add to monthly costs but remove variability from budgets. For fleets covering significant mileage, maintenance packages often prove cost-effective compared to pay-as-you-go servicing.

Example Costings (Illustrative)

For a fleet of 10 medium panel vans (e.g., Ford Transit Custom, Volkswagen Transporter, or equivalent) with a list price around £35,000 each before discount:

| Finance Type | Deposit | Monthly (per van) | Term | End Position |

|---|---|---|---|---|

| Hire Purchase | £3,500 | £620–680 | 48 months | Own outright |

| Finance Lease | £3,000 | £590–650 | 48 months | Return or secondary rental |

| Contract Hire | 3 months | £480–550 | 48 months | Return to funder |

These figures are indicative only. Actual costs depend on specifications, discounts achieved, credit profile, and market conditions at the time of quotation.

What Tax Benefits Apply to Fleet Van Finance?

Tax treatment represents a significant component of total cost. The right structure can materially reduce effective financing costs.

Capital Allowances

Businesses purchasing vans (via hire purchase or outright purchase) claim capital allowances against taxable profits. The Annual Investment Allowance permits 100% first-year deductions on qualifying plant and machinery—including commercial vehicles—up to £1 million annually.

For a £300,000 fleet purchase, a business paying corporation tax at 25% could reduce its tax bill by up to £75,000 in year one, assuming sufficient AIA headroom.

Lease Rental Deductions

For operating leases, rental payments are typically deductible as operating expenses. This spreads the tax benefit across the contract term rather than concentrating it in year one.

VAT Treatment

VAT on van purchases is generally recoverable in full for VAT-registered businesses using vehicles exclusively for business purposes. For leases, VAT on rentals is recoverable on the same basis.

Mixed private/business use complicates recovery—specialist advice is warranted for vehicles that may carry employees for personal journeys.

Benefit in Kind Considerations

If employees use fleet vans for private travel (including commuting), benefit in kind charges apply. For 2024/25, the van benefit charge is £3,960, with additional fuel benefit where private fuel is provided. Structuring fleet policies to prohibit private use can eliminate these charges entirely.

What Credit Requirements Apply for Fleet Van Finance?

Financing five or more vehicles triggers more thorough credit assessment than single-vehicle applications. Funders evaluate several dimensions:

Business Trading History

Most funders require a minimum trading history—typically 2–3 years for unsecured fleet finance. Newer businesses may secure funding with additional security, personal guarantees, or higher deposits. Our team specialise in supporting newly established or infant businesses make their acquisitions! Don’t let you’re infancy in business be a barrier to accessing fleet van finance.

Filed Accounts and Financial Health

Lenders review recent filed accounts, assessing profitability, debt levels, and cash generation. Key metrics include:

- Net profit margin — Demonstrating sustainable trading

- Gearing ratio — Existing debt relative to equity

- Current ratio — Short-term liquidity position

- Debt service coverage — Ability to meet existing and proposed repayments from operating cash flow

Credit History

Business credit files (from agencies like Experian, Creditsafe, and Dun & Bradstreet) inform decisions. Adverse entries—CCJs, defaults, late payments—don’t necessarily preclude approval but may affect terms or require explanation.

Industry Considerations

Some sectors carry higher perceived risk, attracting scrutiny or pricing adjustments. Construction, logistics, and seasonal businesses often face additional questions about revenue stability and contract visibility.

Director/Shareholder Standing

For limited companies, funders may review director credit histories. Outstanding personal issues rarely prohibit fleet finance but can influence terms or deposit requirements.

Frequently Asked Questions About Fleet Van Finance

Can I finance different van models in one agreement?

Yes. Fleet finance commonly accommodates mixed specifications—different models, body types, and even brands—within a single master agreement. This simplifies administration compared to managing multiple separate contracts.

What happens if my mileage requirements change mid-contract?

Most funders permit mileage amendments during the contract term, though this typically triggers a rental adjustment. Increasing mileage raises payments; decreasing may not reduce them proportionally. Early communication with funders helps manage this smoothly.

Can I add vehicles to an existing fleet agreement?

Fleet agreements often include provisions for adding vehicles on aligned terms. Some funders offer “evergreen” or revolving facilities specifically designed for ongoing fleet growth, allowing additions without renegotiating the entire arrangement.

What condition must vehicles be in at contract end?

For leases, vehicles must return in condition consistent with age and mileage—typically assessed against industry-standard guidelines like the British Vehicle Rental and Leasing Association (BVRLA) Fair Wear and Tear guide. Damage beyond these standards incurs rectification charges.

How quickly can fleet van finance be arranged?

For straightforward applications from established businesses, credit decisions often come within 48–72 hours. Complex situations, larger fleets, or unusual structures may require 1–2 weeks. Vehicle delivery timelines—particularly for factory orders—typically exceed finance approval periods.

What security is required for fleet van finance?

Most fleet finance is secured against the vehicles themselves—no additional collateral is required. Larger transactions or higher-risk situations may attract personal guarantee requests, though brokers can often identify funders with lighter security requirements.

Is fleet van finance available for electric vehicles?

Absolutely. Electric van financing has expanded significantly, with some funders offering preferential rates reflecting manufacturer incentives and government policy support. Residual values for EVs remain less predictable than combustion vehicles, which can affect lease pricing.

How to Choose the Right Fleet Van Finance Structure for Your Fleet

Selecting between finance options involves weighing multiple factors against your business priorities:

Choose Hire Purchase if:

- Ownership matters for operational or strategic reasons

- You want to maximise capital allowance claims in year one

- Vehicles will remain in service beyond typical lease terms

- You have strong cash flow to support ownership-level payments

Choose Finance Lease if:

- You want balance sheet assets without full ownership obligations

- Capital allowance timing suits your tax position

- You’re comfortable with fixed-term commitments

Choose Contract Hire if:

- Predictable monthly costs take priority over ownership

- You prefer fixed replacement cycles

- Residual value risk feels uncomfortable

- Maintenance packages appeal for budget certainty

Choose Outright Purchase if:

- You have available cash or favourable existing credit lines

- Maximum flexibility is essential

- You’re confident managing disposal and replacement timing

Why Work with Sorbus Finance for Fleet Van Finance?

Arranging finance for five or more commercial vehicles demands expertise that generalist lenders and direct approaches rarely provide. Sorbus Finance specialises in precisely this space.

Whole-market access — We maintain active relationships with high-street banks, specialist asset financiers, and niche commercial vehicle funders, ensuring proposals reflect genuine market competition rather than a single lender’s pricing. Having access to this variety of fleet van finance, allows our team to support companies of a wide variety of different sizes and trading histories!

Fleet-specific experience — Our team understands the operational realities of running commercial vehicle fleets. We structure deals that align with business cash flows, accommodate staggered deliveries, and provide flexibility for changing requirements.

Transparent comparison — Every proposal includes clear breakdowns of costs, terms, and end-of-contract positions. We explain trade-offs between options rather than pushing predetermined products.

Efficient process — For businesses with established trading histories, we typically deliver initial indicative terms within 24 hours and full credit decisions within a week. Our documentation support minimises administrative burden on your finance team.

Ongoing partnership — Fleet finance isn’t transactional. We monitor your agreements, flag refinancing opportunities, and support end-of-term decisions throughout the vehicle lifecycle.

Next Steps: Getting a Fleet Van Finance Quote

If your business is considering financing five or more vans, the logical starting point is understanding what the market currently offers for your specific situation.

Contact Sorbus Finance for an initial conversation. We’ll discuss your requirements, explain which structures suit your circumstances, and provide indicative terms within 24 hours—no obligation, no hard credit searches at this stage.

Sorbus Finance Website: sorbusfinance.co.uk

Arran Turner is a commercial finance specialist at Sorbus Finance with extensive experience arranging asset finance for UK businesses. He works with companies across multiple sectors to structure fleet funding that supports operational objectives while optimising tax efficiency and cash flow management.